The Disability Tax Credit in Canada: A Practical, Compassionate Guide for Patients and Caregivers

Living with a disability changes far more than your health; it affects your time, your energy, your career, your family, and your finances. The Disability Tax Credit (DTC) was created to ease some of that burden, yet many eligible Canadians have never even heard of it—or they’ve been told they “don’t qualify”.

As a patient advocate, I see the same pattern over and over: people living with very real, very serious functional limitations are denied, or never apply, because the forms are confusing, the rules feel vague, and medical professionals are too rushed to translate lived experience into “CRA language.” My goal with this guide is to simplify what the DTC is, who it’s really for, and how you can apply it in a way that reflects your actual life—not just what’s written in your chart.

If you’re not sure whether you or someone you love might qualify, or you’ve been denied in the past, there is a good chance you’re not alone—and that there are still options.

Many families don’t know the Disability Tax Credit exists — let alone that it could unlock up to 10 years of retroactive refunds. PatientAdvocates.ca can help.

At a Glance: The DTC in 60 Seconds

What it is: A federal non-refundable tax credit for Canadians with severe, prolonged impairments.

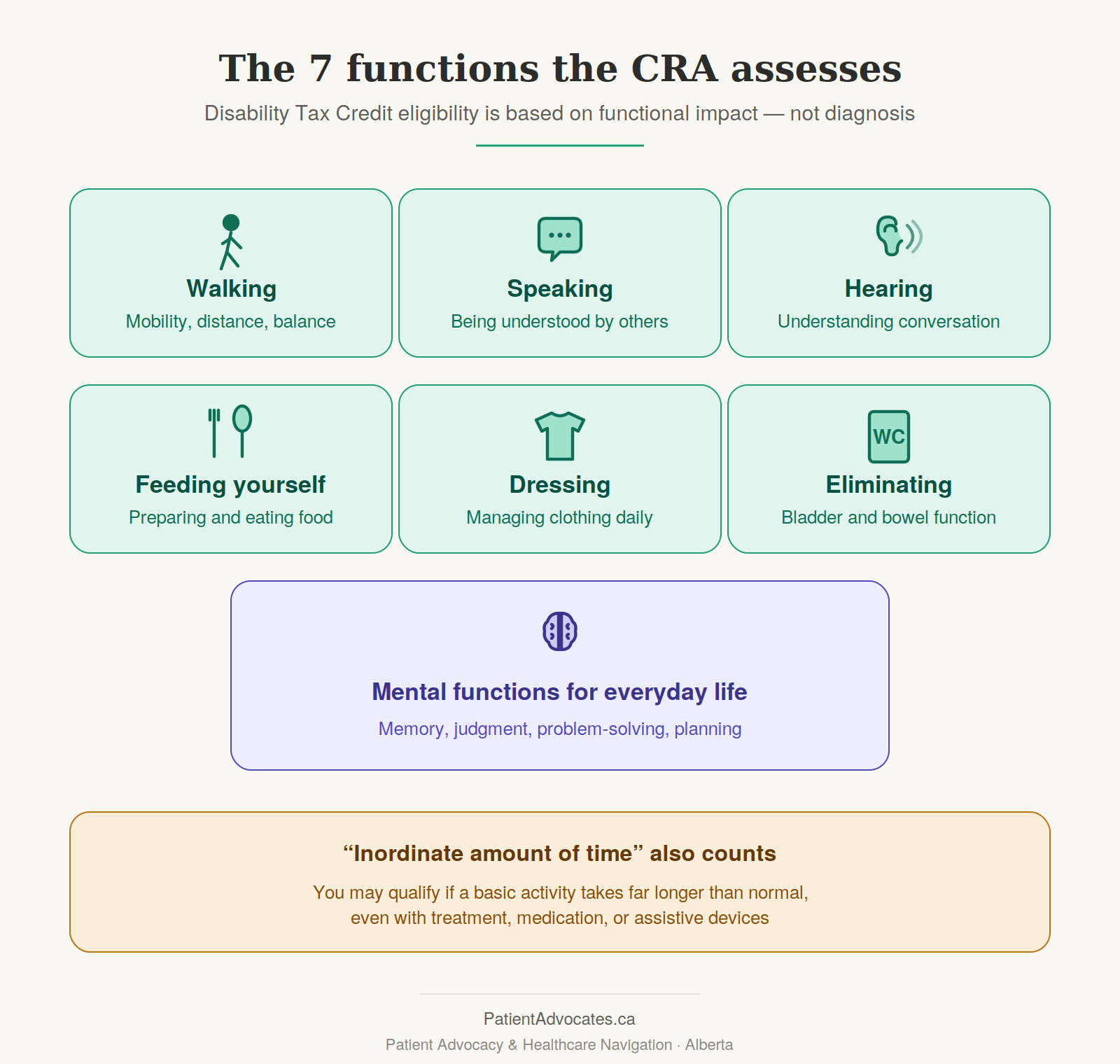

Who qualifies: Based on functional impact across 7 areas of daily living — not on diagnosis alone.

What it unlocks: The RDSP (up to $90,000 in grants/bonds), the Canada Disability Benefit, the Child Disability Benefit, and the Canada Workers Benefit disability supplement.

Retroactive value: Up to 10 years of back credits — often thousands of dollars for the patient or a supporting caregiver.

If you have no income: The credit can transfer to a spouse, parent, adult child, or other supporting family member.

What Is the Disability Tax Credit (DTC)?

The Disability Tax Credit is a federal tax credit that reduces the amount of income tax owing for people who live with significant, long‑term disabilities. It is administered by the Canada Revenue Agency (CRA).

A few key points to understand right away:

It is a non‑refundable tax credit, not a monthly benefit.

It reduces income tax owing. If you do not earn enough income to pay income tax, you will not benefit. However, some or all of it may be transferred to a supporting person (often a caregiver or family member).

Approval for the DTC can open the door to other important financial supports, including the Registered Disability Savings Plan (RDSP), the Canada Disability Benefit, the Child Disability Benefit, and the Disability Supplement of the Canada Workers Benefit.

The DTC is based on how a condition affects daily functioning, not just on the diagnosis itself.

Think of the DTC as recognition of the extra, often invisible costs of living with a disability—lost income, specialized diets, mobility aids, transportation, childcare, home care, and support with daily activities, among many others.

Update: Streamlined DTC Applications (Spring 2026)

Breaking News: The federal government’s Spring 2026 Economic Update introduces a massive reform to simplify the Disability Tax Credit (DTC) application process.

To reduce medical paperwork barriers, the Canada Revenue Agency (CRA) is launching a streamlined application process for individuals with a formal diagnosis of specific, well-established, long-lasting conditions. For these cases, qualifying healthcare practitioners only need to certify the diagnosis itself, bypassing the exhaustive, detailed logs regarding daily living functional impacts.

Fast-Tracked Conditions Include:

Cognitive/Neurological: Alzheimer’s disease, Dementia, advanced Parkinson's, and Huntington disease.

Developmental/Genetic: Level 3 Autism Spectrum Disorder, Down syndrome, Angelman syndrome, and Patau syndrome.

Physical/Mobility: ALS (Lou Gehrig's), Paraplegia, Quadriplegia, and severe Cerebral Palsy.

Sensory/Organ: Bilateral blindness, profound bilateral hearing loss, and Class IV Cardiac impairment.

While this change drastically lowers administrative hurdles, ensuring your medical team completes the new certification fields accurately is still critical to avoid processing delays.

For the complete official listing of eligible conditions, consult the Spring Economic Update 2026: Supplementary Tax Measures. You can also read community navigation analysis via the March of Dimes Canada Reform Statement.

Who Can Qualify for the DTC?

You may qualify for the DTC if you have a severe and prolonged impairment that has lasted, or is expected to last, at least 12 months and significantly affects your basic daily functioning.

The CRA assesses eligibility in several key ways.

1. Marked Restriction

You may be considered to have a marked restriction if you are unable to perform one or more basic activities of daily living, or take an inordinate amount of time to do so, even with appropriate treatment, medication, or assistive devices.

The CRA looks at seven core functions:

Walking

Speaking

Hearing

Feeding yourself

Dressing

Eliminating

Mental functions necessary for everyday life (for example: memory, judgment, planning, problem‑solving, understanding and using information)

“Inordinate amount of time” is one of those phrases that sound technical but describe something many people live with: what used to take you minutes now takes you much longer, or costs you so much energy that you pay for it later in pain, fatigue, or a cognitive crash.

You don't need a "severe" diagnosis to qualify. You need a clear picture of how a condition affects these seven daily functions.

2. Significant Restriction

You might not be fully restricted in one functional area, but you may be substantially limited all or most of the time.

For example, you might still be able to walk, but only short distances, using a device, with frequent breaks, or at the cost of intense pain or exhaustion. Or you may be able to concentrate for brief periods but find it impossible to manage complex tasks, multitask, or keep up with regular work demands.

3. Life‑Sustaining Therapy

You may qualify under life‑sustaining therapy if you require therapy that:

Is essential to sustain life

Takes 14 hours or more per week

Must be performed at least three times per week

Insulin therapy for certain people with diabetes is a common example, but there are others.

4. Cumulative Effect of Significant Limitations

For many of my clients, this is the most accurate category.

You may have multiple mild or moderate impairments that, together, significantly limit your day‑to‑day functioning. On paper, each one might not seem “severe enough,” but in real life, the combination can be absolutely disabling.

This is especially relevant for people living with:

Chronic illness (such as ME/CFS or fibromyalgia)

Long COVID

Autoimmune conditions

Cancer‑related impairments and treatment side‑effects

Chronic pain and fatigue

Neurological or degenerative conditions

Serious mental health conditions such as major depressive disorder, anxiety disorders, PTSD, or severe ADHD

Mild, intermittent, or well‑controlled symptoms that have little impact on daily functioning generally do not qualify, but many people are told their condition is “mild” based solely on lab results or snapshots in time, rather than on the reality of an average day or week.

Common Conditions That May Qualify

The DTC is never based on diagnosis alone. Two people with the same diagnosis can have very different outcomes—one may qualify, the other may not—depending on how their condition actually affects daily life.

That said, some conditions commonly associated with DTC eligibility include:

Diabetes requiring intensive insulin therapy

Multiple sclerosis

Stroke and related functional impairment

Autism spectrum disorder

Severe ADHD with significant functional impact

Major depressive disorder and severe anxiety disorders

Cancer‑related disability and treatment side‑effects

Chronic fatigue syndrome and other chronic pain conditions

Neurological and degenerative diseases such as Parkinson’s or ALS

If you’re not sure whether your situation is “severe enough,” that is often an important signal to explore the criteria more closely with someone who understands both the CRA language and the realities of disability.

The DTC → RDSP → CDB Chain (And Why 2026 Matters)

In 2026, three federal disability programs work together more powerfully than ever:

The Disability Tax Credit (DTC) is the gateway. Without it, none of the other doors open.

The RDSP is the wealth-building tool unlocked by DTC approval.

The Canada Disability Benefit (CDB) — Canada’s newest federal benefit, launched in July 2025 — provides up to $200 per month to working-age DTC holders.

Here is the part most people miss: money sitting in your RDSP and money you withdraw from it do not count against your Canada Disability Benefit eligibility. The RDSP was specifically designed to be exempt for federal benefit purposes.

This means the DTC, RDSP, and CDB are not separate puzzles. They are one strategy. And the order in which you tackle them matters.

How Do You Apply for the Disability Tax Credit?

You apply for the DTC by completing and submitting Form T2201 – Disability Tax Credit Certificate to the CRA.

The form has two main parts:

Part A – Patient or Representative

This section is completed by:

The person with the disability, or

Their legal representative (for example, a parent or power of attorney)

It covers basic personal information and allows you to authorize someone, such as a patient advocate, to speak with the CRA on your behalf.

Part B – Medical Practitioner

This section must be completed by a qualified medical professional, such as:

Physician or nurse practitioner

Psychologist

Occupational therapist

Physiotherapist

Optometrist

Audiologist

Speech-language pathologist

This is the most crucial part of the application — and it's also where most applications get into trouble. Approvals and denials very often come down to how clearly daily functioning is described here. I cover what makes this section succeed (or fail) in detail further down, in How a Patient Advocate Can Help.

How to Submit

The completed T2201 can be submitted in two ways:

Digitally, by your medical professional through the CRA's online portal, using a reference number you generate in your CRA MyAccount after completing Part A

By mail, with the printed form sent to the CRA at the address listed on the form

Once submitted, the CRA typically takes around 8 weeks to issue an initial decision on the application, though more complex files can take longer.

What If the Disabled Person Has Little or No Income?

If the person living with the disability has little or no taxable income, the DTC can often be transferred to a supporting person so it does not go to waste.

This is one of the most misunderstood aspects of the Disability Tax Credit.

Because the DTC is a non‑refundable tax credit:

It cannot generate a refund beyond what you have paid in tax.

If you have no taxable income (for example, if you only receive non‑taxable benefits), you may not benefit directly.

However, that does not mean the credit is useless.

Transferring the DTC to a Caregiver

If the person with the disability cannot use the full credit, some or all of it can often be transferred to a supporting person and is claimed as the Canada Caregiver Credit.

Who Can Be a Supporting Person?

A supporting person may include:

A spouse or common‑law partner

A parent or step‑parent

An adult child

A sibling

Another relative who provides regular support

A friend - if they pay more than 50% of the expenses of the disabled person and cohabitate

To qualify as a caregiver for transfer purposes, you generally need to:

Provide financial or personal support

Be responsible for some of the person’s basic needs (such as food, shelter, or care)

In some cases, you do not have to live in the same home, especially if you are an adult child supporting aging parents.

What Does the Caregiver Receive?

When the DTC is transferred:

The caregiver can use the disability amount to reduce their own income tax.

The credit can often be applied retroactively for eligible years.

This can result in substantial tax refunds—sometimes thousands of dollars.

This can be especially impactful for:

Parents of disabled children

Spouses supporting a disabled partner

Adult children supporting disabled or aging parents

This is one way the tax system acknowledges that disability is rarely experienced by a single person; it usually affects the whole family.

Retroactive Benefits: Going Back Up to 10 Years

If the DTC is approved, it may be applied retroactively to up to 10 prior tax years, depending on the medical evidence.

Retroactivity can apply whether:

The person with the disability is claiming the credit, or

A caregiver is claiming the transferred amount

Many families have missed out simply because nobody told them they might be eligible years ago. In some cases, a successful DTC application today can lead to a significant refund for past tax years in which the person already met the criteria.

Other Programs the DTC Can Unlock

One of the most powerful aspects of DTC approval is that it can open doors to other programs and supports.

These may include:

Registered Disability Savings Plan (RDSP) – A long‑term savings plan where the federal government often contributes significantly more than you do through grants and bonds, within certain income limits and contribution rules. For many people with disabilities, this is one of the most misunderstood yet powerful financial tools available.

Child Disability Benefit – A tax‑free monthly payment of up to $3,173 per year as of 2024/2025 to families who care for a child under 18 who qualifies for the DTC.

Canada Disability Benefit - As of July 2025, eligible individuals with low or modest incomes may be able to apply for this new benefit.

Canada Workers Benefit (CWB) Disability Supplement provides an additional payment of $784 per year for eligible working individuals.

Certain additional medical expenses and deductions can be claimed once you have DTC approval.

Home Buyers’ Amount for eligible expenses incurred for renovations that make a home more accessible.

Provincial disability supports – In some provinces, DTC status can support access to additional provincial benefits or programs.

Tax and estate planning opportunities – For example, structuring support for an adult child with a disability, or planning for the financial security of a partner living with a chronic condition.

If you qualify for the DTC, it is worth exploring whether you also qualify for a Registered Disability Savings Plan or other related programs. In many cases, the RDSP alone can meaningfully shift a person’s long‑term financial stability.

Why Are So Many Disability Tax Credit Applications Denied?

If you have been denied, you are not alone—and it does not automatically mean you do not qualify.

Applications are often denied because of issues with how the story is told on paper, not because the person’s challenges are not real or serious.

Common problems include:

Forms that focus on diagnosis instead of function

Vague or overly brief descriptions of daily limitations

Medical practitioners who underestimate the impact, or who worry about adding financial burden by charging for form completion, in case their patient is denied.

Incomplete, inconsistent, or improperly submitted documentation

CRA reviewers misunderstand fluctuating or invisible disabilities, especially conditions that vary from day to day

Paperwork filled out incorrectly or with missing sections

Another major issue is that many medical professionals:

Are not informed about the outcome of the applications they complete, so they rarely receive feedback about what was “missing.”

Do not have the time or systems to fully document a patient’s day‑to‑day challenges, especially when those challenges are not easily captured in lab results or short office visits.

This is why I often encourage clients to:

Write out, in detail, what daily life looks like and how long tasks take.

Draft answers in pencil or in a separate document for the medical section that they can share with their provider.

Bring specific examples of how their condition affects them most days, not just on their best days.

Medical records show what is clinically measurable. Life at home shows what is actually lived. When we bring those two together, a much clearer picture emerges—one that reflects not only your diagnosis, but its real impact on the basic activities the CRA assesses.

What Can I Do If I Am Denied?

A denial can feel like a judgment on your experience, but it is often a reflection of the paperwork — not your worth, and not the legitimacy of your disability. Many of the strongest, most clearly eligible files I've worked on were denied the first time around. The good news: a denial is rarely the final word.

Here's what you can do:

1. Request a copy of what your medical professional submitted. This is the single most important step, and one most people skip. Once you can see what the CRA saw, you can identify inaccuracies, missing details, or sections that were left incomplete. You have a right to this information.

2. Ask your provider to clarify or expand on key points. Most denials hinge on vague or thin descriptions of daily functioning — especially around how long tasks take, how often you are limited, and what support you need. A short follow-up document from your provider can often address the specific gaps the CRA flagged.

3. Request a formal review (Request for Redetermination). This is an informal review process where you submit new or updated medical information and ask the CRA to take a second look. There's no strict deadline, but the CRA can refuse if you wait too long — so move quickly. You'll have up to a year to complete the process once you start.

4. File a Notice of Objection within 90 days. If a review doesn't resolve the denial — or if you'd rather go straight to a formal appeal — you have 90 days from the date on your Notice of Determination to file a formal objection. This is taken seriously and triggers a fresh review by the CRA's Appeals Branch. DTC objections are classified as "low complexity" by the CRA, with current resolution times averaging around four months from submission.

5. Get help from someone who understands both the medical and CRA sides. A patient advocate, an experienced disability lawyer, or in some cases your medical practitioner can help identify exactly where the original application fell short and how to rebuild it for success.

An initial denial is not the end of the road. Many successful approvals happen on review or appeal — often when someone takes a fresh look at how the original application was framed.

Corinne Hewko, RN — Patient Advocate & Healthcare Navigator, founder of PatientAdvocates.ca, serving clients across Edmonton, St. Albert, and Alberta.

How a Patient Advocate Can Help

My role as a professional Patient Advocate is to bridge the gap between lived experience and medical paperwork — and with the DTC, that gap is often the difference between approval and denial.

In practical terms, I:

Listen carefully to your story and help you identify where your daily functioning aligns with the CRA's criteria.

Recognize gaps in your documentation or application that could lead to a denial.

Help you prepare detailed, accurate information for your medical professional, so they are not left to dig through years of chart notes on their own.

Guide you through the application or appeal process, step by step.

What this looks like in practice: the T2201

The single most important section of any DTC application is the medical practitioner portion of Form T2201 — and it's also where most applications get into trouble. Approvals and denials often come down to how daily functioning is described here. Vague statements like "has chronic pain" or "has depression" usually are not enough. What the CRA needs is a clear, concrete picture of what daily life looks like:

How long does it take you to get dressed or bathe?

Can you safely manage your medications on your own?

How often do you forget appointments or steps in a task?

How far can you walk on a typical day, and what happens if you push past that?

What happens after a "big" effort — do you crash the next day?

Here's the workflow I typically use with clients:

I review your medical history and, more importantly, your story of daily life: what a "good day" and a "bad day" look like, what you've had to give up, and where you need help.

Together, we map your real-world functional challenges to the CRA's language and categories.

I then draft the relevant portions of the medical section in pencil or as a reference document that you can bring to your medical professional, along with the blank T2201 or a CRA reference number for electronic submission.

This is not about telling your provider what to write; it's about making it easier for them to see you clearly and capture the details that rarely fit into a 10–15-minute appointment. Most physicians are not trying to block access to the DTC — they are juggling time pressures, heavy documentation demands, and forms they receive very little training on.

Providing a structured, accurate description of your daily functioning can:

Decrease the overwhelm for your medical professional

Reduce the risk of inaccuracies or incomplete sections

Increase the chance that your application reflects your actual level of impairment

What this costs — and why our model is different

Importantly, I will not encourage you to pay for medical form completion (often between $100–$250) unless we first have a clear, honest sense that your situation likely meets the DTC criteria. Your time, money, and energy are valuable; any application should respect that.

A quick word about those companies advertising "DTC refund help" online: most charge 25–30% of your refund. On a 10-year retroactive claim worth $25,000, that's $6,000–$7,500 out of money the federal government intended for you.

At PatientAdvocates.ca, we only charge hourly. Because we coach you through what you can do yourself, even our most complex files — the ones where we attend doctor's appointments with you — typically come in under $1,000 total. Because we're paid for our time, we have no incentive to push an application we don't believe in.

Final Thoughts: You Are Asking for Fairness, Not Favour

The Disability Tax Credit is not a handout or an act of charity. It is an acknowledgment that disability has real, ongoing costs—financial, emotional, and practical—that are often carried quietly by patients and families.

If you:

Live with a disability and have little or no income, or

Support a loved one who lives with a disability

You may still benefit significantly from the DTC, especially through caregiver transfer and retroactive claims.

You are not asking for special treatment. You are asking for fairness.

If this process feels overwhelming, you do not have to manage it alone. I offer a complimentary consultation to review your situation, help assess potential eligibility, and discuss whether applying (or re‑applying) for the Disability Tax Credit makes sense for you or your loved one. Together, we can make sure your lived reality is reflected on paper—and that you receive the support you are entitled to.

If you’d like help, please reach out, and we can take the next step together.

👉Book a free, no-obligation discovery call to find out exactly what you may be entitled to.

This article is for general information only and does not replace personalized financial, tax, or legal advice. DTC rules, contribution limits, and benefit thresholds are reviewed and indexed annually by the Government of Canada. For current figures, always confirm with the Canada Revenue Agency or a qualified professional.

Frequently Asked Questions

Who qualifies for the Disability Tax Credit in Canada?

Individuals with a severe and prolonged impairment in physical or mental functions—lasting or expected to last at least 12 months—certified by a medical practitioner using Form T2201, may qualify for the DTC.

Does the Disability Tax Credit affect my AISH or CPP-Disability?

No. The DTC is a federal tax credit and does not reduce AISH, CPP-Disability, or other provincial and federal disability benefits. In Alberta, AISH recipients can claim the DTC (or transfer it to a caregiver) without any impact on their monthly support.

Can I still qualify if I'm able to work?

Yes. The DTC is based on functional impairment in basic activities of daily living, not on employment status. Many people who work — sometimes with significant accommodations or reduced hours — still meet the criteria, particularly under the cumulative effect or significant restriction categories.

What if my condition fluctuates from day to day?

Fluctuating and invisible disabilities are explicitly recognized by the CRA. The standard is whether the limitation exists "all or substantially all of the time" — which can absolutely include conditions with bad days, crashes, or flares. The application needs to describe what your average and worst days look like, not just your best.

Do mental health conditions qualify for the DTC?

Yes. Severe and prolonged mental health conditions — including major depressive disorder, severe anxiety disorders, PTSD, severe ADHD, and others — can qualify under the "mental functions necessary for everyday life" category. The key is documenting functional impact on memory, judgment, problem-solving, and daily management.

Can my doctor charge a fee for completing the T2201?

Yes. Form completion is not covered by provincial health insurance, and most physicians charge between $100 and $250 for the T2201. This is one reason it's worth assessing eligibility carefully before requesting form completion — to avoid paying for a denial.

Can the DTC be transferred if I don't qualify as a caregiver in the traditional sense?

Yes, in many cases. Adult children supporting aging parents, siblings providing regular support, and even non-cohabitating family members may qualify as a supporting person for transfer purposes — provided they contribute meaningfully to the person's basic needs. You don't always have to live together.

How far back can the DTC be applied?

Up to 10 prior tax years, depending on when the impairment began and what the medical evidence supports. Retroactive claims can result in refunds of several thousand to tens of thousands of dollars — for either the person with the disability or a transferring caregiver.

What if I've been denied the DTC before?

A denial is not the final word. You can request a copy of what your medical practitioner submitted, supply additional medical information, file a formal Notice of Objection within the allowed timeframe, or work with a patient advocate to rebuild the application. Many successful approvals happen on review or appeal.

Does the DTC unlock the new Canada Disability Benefit?

Yes. As of July 2025, DTC approval is the gateway to the Canada Disability Benefit — up to $200/month for eligible working-age Canadians with low or modest income. DTC approval is also required to open a Registered Disability Savings Plan.

Related resources for Albertans

The Disability Tax Credit rarely stands alone. For most people, it's the entry point into a broader set of federal and provincial programs that work together — and knowing what exists is half the battle. Here are the most useful starting points:

Federal programs and benefits

Disability Tax Credit (CRA overview) — eligibility, application, and current amounts

Form T2201 (CRA) — the official Disability Tax Credit Certificate

Registered Disability Savings Plan (RDSP) — the long-term savings plan DTC approval unlocks

Canada Disability Benefit — federal monthly benefit for working-age DTC holders

Child Disability Benefit — tax-free monthly payment for families caring for a child with a disability

CPP-Disability — Canada Pension Plan disability benefit

Canada Workers Benefit – Disability Supplement — additional payment for eligible working individuals

Transferred DTC to a supporting person — how caregivers can claim the credit

Alberta provincial programs

Assured Income for the Severely Handicapped (AISH) — Alberta's primary disability income support program

Alberta Adult Health Benefit — health benefits for low-income Albertans

Persons with Developmental Disabilities (PDD) — supports for adults with developmental disabilities

Filing an objection or appeal

Notice of Objection (CRA) — formal process for disputing a denial

Disability Tax Credit Promoters Restrictions Act — federal law capping fees charged by DTC application services

Related reading on this site

The RDSP in Canada: Free Government Money for Anyone Approved for the DTC Our full guide to the RDSP, including the catch-up window for late starters