The 2026 RDSP Guide for Albertans: How to Claim the Free Government Money You're Owed

A plain-language guide to the Registered Disability Savings Plan in Canada — who qualifies, how to get up to $90,000 in government grants and bonds, how the 10-year catch-up rule works, and how the RDSP pairs with AISH, CPP-Disability, and the new Canada Disability Benefit in 2026.

The Registered Disability Savings Plan (RDSP) is a federal savings plan for Canadians approved for the Disability Tax Credit, offering up to $90,000 in government grants and bonds — even with little or no personal contribution.

If you, or someone you love, has been approved for the Disability Tax Credit (DTC) in Canada, there is one financial tool you need to understand — and the sooner the better.

It’s called the Registered Disability Savings Plan (RDSP), and in 2026 it remains one of the most generous, most underused, and most poorly explained programs in this country. Fewer than one in three eligible Canadians have opened one. The rest are leaving real, life-changing money on the table.

As a patient advocate and healthcare navigator working with families across Alberta — and through our partners across British Columbia — I see this every week. The RDSP isn’t complicated because the program is bad. It’s complicated because it’s bureaucratic, inconsistently explained at the bank, and rarely framed in the way that matters most for real people: as free government money you may be entitled to.

This guide breaks it down in plain language, with a special focus on late starters, low-income individuals, and anyone receiving disability benefits like AISH or CPP-Disability in Alberta.

At a Glance: The RDSP in 60 Seconds

What it is: A long-term, tax-deferred savings plan for Canadians approved for the DTC.

Who can open one: Anyone with DTC approval, a SIN, Canadian residency, and who is under age 60.

The big incentive: The Government of Canada can deposit up to $90,000 into your plan over your lifetime through grants and bonds.

Even with $0 contributions: Low-income individuals may receive up to $20,000 in bonds without contributing a dollar.

Catch-up window: You can claim up to 10 years of missed grants and bonds retroactively — but only if you open the plan.

Newest connection (2026): The Canada Disability Benefit (CDB) — up to $200/month for working-age DTC holders — pairs with the RDSP without clawback.

What Is an RDSP — and Why Does It Matter?

The Registered Disability Savings Plan was designed by the federal government to help Canadians with disabilities build long-term financial security. What makes it different from an RRSP, TFSA, or any savings account at your bank is one simple fact:

The government contributes far more than most individuals ever could.

Through two specific programs — the Canada Disability Savings Grant and the Canada Disability Savings Bond — eligible Canadians can receive tens of thousands of dollars in their plan, often with little or no money of their own.

For families I work with in Edmonton, St. Albert, Calgary, and across rural Alberta, that money has meant the difference between worrying about every prescription co-pay and finally feeling some financial breathing room.

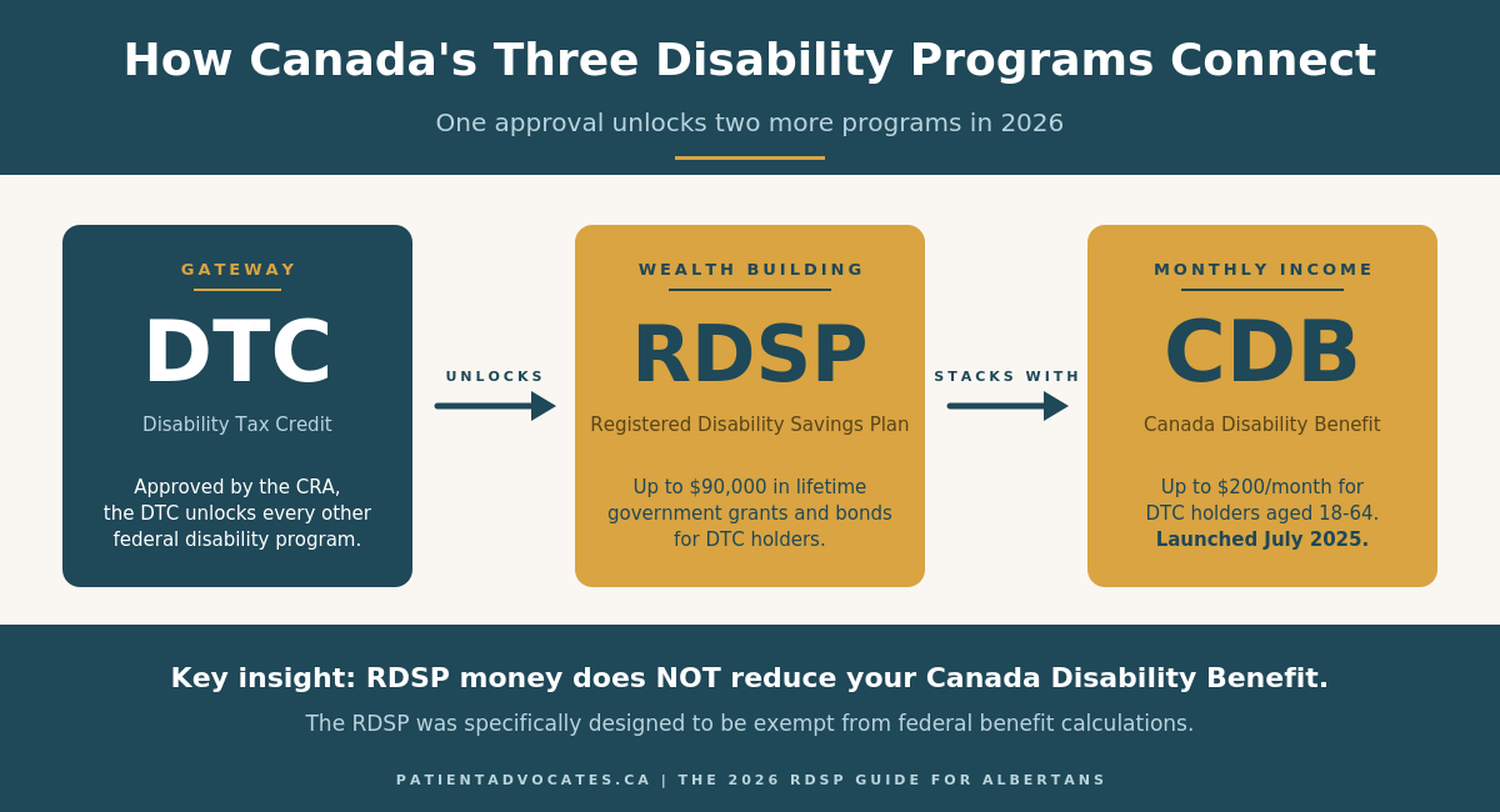

The DTC → RDSP → CDB Chain (And Why 2026 Is the Year to Pay Attention)

In 2026, three federal disability programs work together more powerfully than ever:

The Disability Tax Credit (DTC) is the gateway. Without it, none of the other doors open.

The RDSP is the wealth-building tool unlocked by DTC approval.

The Canada Disability Benefit (CDB) — Canada’s newest federal benefit, launched in July 2025 — provides up to $200 per month to working-age DTC holders.

Here is the part most people miss: money sitting in your RDSP and money you withdraw from it do not count against your Canada Disability Benefit eligibility. The RDSP was specifically designed to be exempt for federal benefit purposes.

This means the DTC, RDSP, and CDB are not separate puzzles. They are one strategy. And the order in which you tackle them matters.

Who Can Open an RDSP

To qualify, the beneficiary must:

Be approved for the Disability Tax Credit (DTC)

Be a Canadian resident for tax purposes

Have a valid Social Insurance Number (SIN)

Be under age 60 when contributions are made (the plan must be opened by December 31 of the year the beneficiary turns 59)

A detail almost no one explains at the bank: if a beneficiary later loses DTC eligibility, the RDSP can usually remain open. Don’t walk away from a plan because of a temporary status change without first getting proper advice.

How an RDSP Actually Grows

There are three ways money can be contributed to an RDSP. The third is where most of the magic happens.

1. Personal Contributions

Lifetime contribution limit: $200,000

No annual minimum — you can contribute $0 in any given year

Not tax-deductible (unlike an RRSP)

Anyone can contribute: the beneficiary, parents, family, friends, even neighbours

You can contribute at any pace — or not at all. This flexibility matters enormously for people on fixed incomes.

2. The Canada Disability Savings Grant (CDSG)

This is a matching grant the government deposits when you contribute. The match rate depends on your family income (using your tax return from two years prior — so 2024 income drives 2026 grants).

Lower-income households: the government may match every $1 you contribute with $3 — up to a maximum of $3,500 per year

Higher-income households: $1-for-$1 matching, up to $1,000 per year

Lifetime maximum: $70,000

Grants are paid until December 31 of the year the beneficiary turns 49

In real terms: for many Albertans I work with, a $1,500 contribution becomes $5,000 the same week. Run your numbers using the official Government of Canada grant and bond calculator →

3. The Canada Disability Savings Bond (CDSB)

This is the part that changes lives — and it’s the part the bank rarely highlights.

Up to $1,000 per year deposited by the government

Lifetime maximum: $20,000

No personal contribution required — you receive the bond automatically if you’re eligible and your taxes are filed

Available to low- and modest-income individuals/families

Read that again: you can receive up to $20,000 from the federal government, simply by opening the plan and filing your taxes. No contribution. No catch. No clawback against AISH or CPP-D.

The Catch-Up Opportunity: 10 Years of Missed Money

This is the single most overlooked feature of the RDSP, and it’s the one I want every Albertan family to internalize.

If you’ve been DTC-approved in any of the past 10 years — even retroactively — you may be eligible to claim up to 10 years of missed grants and bonds when you open and contribute to your RDSP.

That means the moment you open the plan, you can sometimes unlock:

Up to $10,500 in grant in a single year (the annual carry-forward maximum), plus

Up to $11,000 in carry-forward bond

But here is the catch: carry-forward only applies once the plan is open. Every year you delay opening your RDSP is a year that potentially falls off the back of the 10-year window.

If you take one thing from this article: open the plan now, even with $0. The clock on retroactive grants and bonds starts on the day the plan is created, not the day you have spare cash.

RDSP Strategy for Late Starters (Approved for DTC in Your 40s or 50s)

For my clients who get the DTC later in life — after a stroke, an MS diagnosis, long COVID, a late-onset autism diagnosis, or a chronic pain condition that finally gets formally documented — the RDSP playbook shifts.

It is no longer primarily a savings plan. It becomes a government benefit capture plan.

Here’s how I coach late starters through it:

1. Open Immediately — Even With No Money

Opening the RDSP starts the clock on retroactive grants and bonds. Delay equals lost free money. Period.

2. Prioritize Government Money Over Personal Savings

Don’t try to maximize the $200,000 lifetime contribution limit. For most late starters, that’s neither realistic nor smart. Instead:

Contribute only enough each year to trigger the maximum grant for your income level

Capture every available bond you’re eligible for

Don’t put dollars in that won’t attract a match — they become “unassisted contributions” that lock you in without earning you anything

3. Work Backwards From Age 59

Grants and bonds stop at the end of the year the beneficiary turns 49 (with a 10-year carry-forward window after that). Personal contributions stop at age 59. So:

Count how many eligible years remain

Maximize each one strategically

For someone approved at age 55, timing matters far more than contribution size

4. Avoid Early Withdrawals (The 10-Year Repayment Rule)

This is where people get burned. Withdrawals within 10 years of receiving any grant or bond can trigger a repayment of those government deposits.

Rule of thumb: plan to leave the money in the plan for at least 10 years after the last government contribution.

Bottom Line for Late Starters

It’s not about how much you save. It’s about how much government support you can capture before age 60, with up to 10 years of retroactive eligibility working in your favour.

RDSP and Provincial Disability Benefits in Alberta

I have clients that collect AISH in Edmonton, St. Albert, Calgary, Red Deer and Lethbridge who avoided applying for the RDSP, as they were afraid that it would cost them their benefits.

However, in the vast majority of cases, it does not. Here’s why:

RDSP and AISH (Alberta)

RDSP assets are fully exempt when AISH calculates eligibility

Withdrawals are typically exempt when structured correctly

The RDSP does not reduce your AISH cheque

This makes the RDSP one of the safest financial tools available to AISH recipients — and one of the very few wealth-building options that doesn’t put your monthly support at risk.

Advocacy note: Administrative errors do happen. I’ve seen RDSP withdrawals incorrectly recorded as “income” by overworked caseworkers. Always keep your paperwork, and don’t hesitate to push back if your AISH file is suddenly flagged after an RDSP transaction.

RDSP and CPP-Disability (CPP-D)

No impact on CPP-D eligibility

CPP-D payments are not reduced by RDSP withdrawals

The RDSP works alongside CPP-D for long-term financial stability

RDSP and the New Canada Disability Benefit (CDB)

This is brand new for 2026 and worth repeating: RDSP money does not count as income when Service Canada calculates your CDB amount. The two benefits stack.

What About BC Residents?

While my practice is based in Alberta, I work closely withPatient Pathways Healthcare Navigation in British Columbia for clients on Vancouver Island, the Lower Mainland, the Cowichan Valley, and across the province. RDSP rules are federal and apply identically in BC — but provincial benefit interactions (such as PWD in British Columbia) work a little differently. For BC residents reading this, the same federal grants and bonds apply, and we’re happy to point you toward the right BC-based advocate.

Common RDSP Myths — A Quick Reality Check

“I need money to open one.” No. You can open an RDSP with $0 and still receive bond payments.

“It will affect my disability benefits.” In almost every case, no. RDSPs are exempt from AISH, CPP-D, and the new Canada Disability Benefit.

“It’s only for kids.” Not true. Adults — including people approved in their 40s or 50s — can capture significant value, and often more efficiently than parents of young children.

“It’s too complicated.” It’s bureaucratic, but absolutely manageable with the right guidance. That’s exactly why patient advocates and healthcare navigators exist.

“My bank will explain it to me.” Some will. Many won’t. RDSPs are time-consuming for front-line bank staff, and the carry-forward calculations are complex. Walk in informed — or walk in with an advocate.

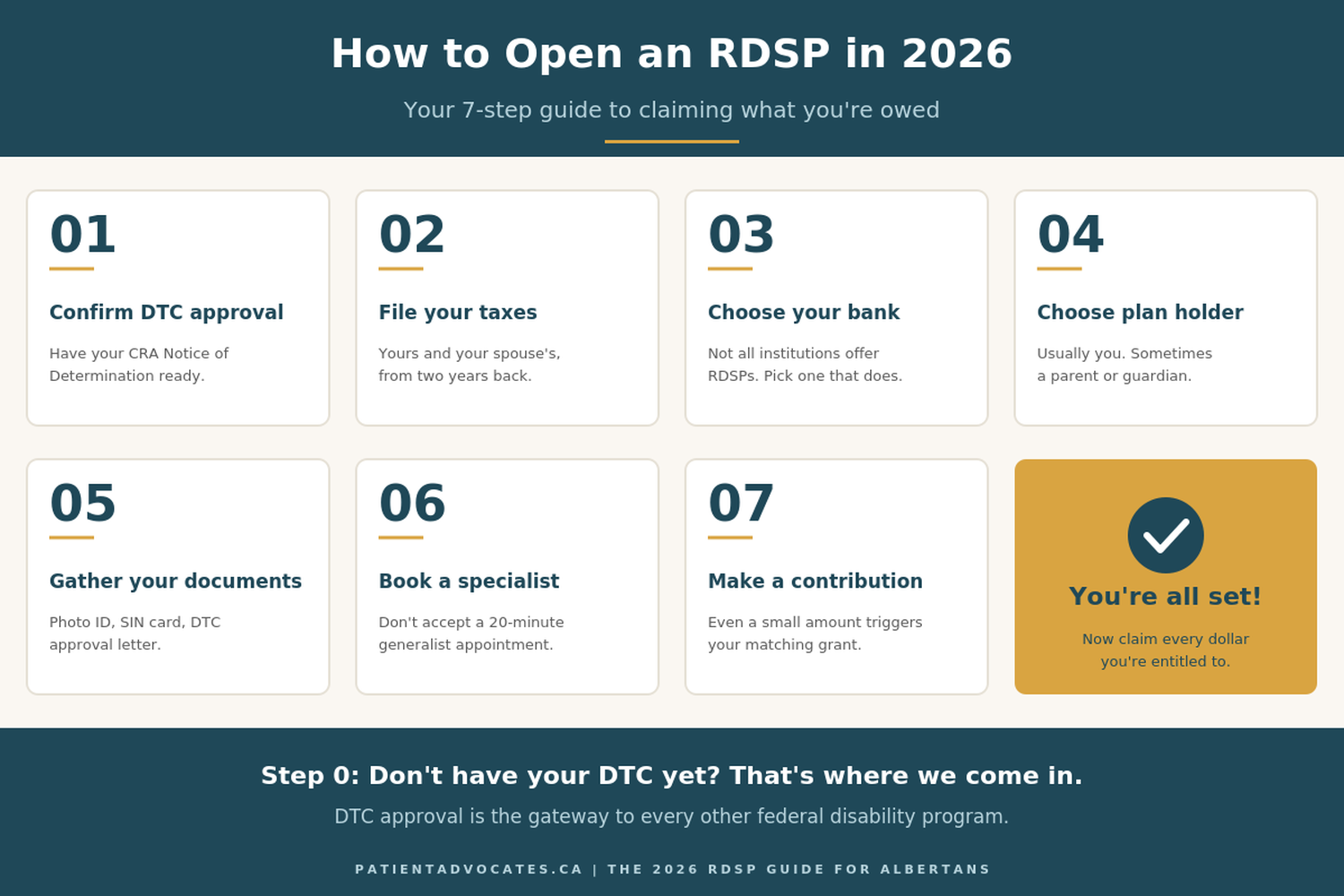

How to Open an RDSP — The Practical Steps

Confirm DTC approval. If you don’t have it yet, this is step zero. (We help clients with this constantly.)

File your taxes — yours, and your spouse’s if applicable. Grants and bonds rely on filed returns from two years prior.

Choose a financial institution that offers RDSPs. Not all do, and not all do it equally well. The major Canadian banks, several credit unions, and some specialty firms offer them.

Decide who will be the plan holder. This is straightforward for capable adults but more complex when capacity is in question.

Gather your documents: photo ID, SIN card, DTC approval letter (or recent Notice of Assessment showing DTC).

Book the appointment. RDSP openings often need a specialized banker — don’t accept a 20-minute generalist appointment.

Make a small contribution, if possible, to trigger the matching grant for the current year, plus any carry-forward you’re eligible for.

Frequently Asked Questions

Do I need to be approved for the DTC before I open an RDSP?

Yes. DTC approval is the gateway. If you suspect you may qualify and haven’t applied, that should be your first step.

How much can I receive in grants and bonds total?

Up to $70,000 in grants and $20,000 in bonds over a lifetime — a combined federal contribution of up to $90,000.

Will my AISH be affected if I open an RDSP?

In Alberta, RDSP assets and properly-structured withdrawals are exempt from AISH calculations. Always confirm your withdrawal structure with someone who understands the rules.

Can I still benefit if I’m in my 50s?

Yes — and the carry-forward feature can be especially powerful for late starters. The earlier you open, the more retroactive years you can claim.

What happens if I lose DTC eligibility later?

The plan can usually remain open, though grants/bonds pause. Don’t close the plan without advice.

Can someone else open the plan for me?

Yes — parents, guardians, or qualifying family members can be the plan holder for adults whose capacity is in question. The rules around this have changed for the better in recent years.

Does the Canada Disability Benefit affect my RDSP?

No. CDB and RDSP are designed to work together. RDSP amounts don’t reduce your CDB, and CDB deposits placed into your RDSP can attract matching grants.

You Don’t Have to Figure This Out Alone

Here’s the truth I tell every family in my office: the RDSP is one of the best things the federal government has built for Canadians with disabilities — and one of the worst-explained. It’s not your job to be an expert in carry-forward calculations, AISH exemption rules, and Canada Disability Benefit interactions. This is where we here at PatientAdvocates.ca can help you:

Apply for and successfully secure the Disability Tax Credit (the gateway to everything)

Coordinate RDSP opening with the right financial institution and the right banker

Calculate carry-forward entitlements so no eligible year is missed

Apply for the Canada Disability Benefit alongside DTC and RDSP

Navigate AISH and CPP-Disability so your provincial benefits aren’t put at risk

Support family caregivers acting as RDSP plan holders

We work in person across Edmonton, St. Albert, Sherwood Park, and surrounding communities, and virtually with clients across all of Alberta and Canada. For our friends in British Columbia — including Vancouver, Victoria, the Cowichan Valley, and the Lower Mainland — we partner withPatient Pathways Healthcare Navigation.

Ready to claim what’s yours?

If you’ve been putting off opening an RDSP because the paperwork felt overwhelming, or because the bank made it sound complicated, or because you’ve been told the wrong thing about how it interacts with your benefits — let’s talk.

👉Book a free, no-obligation discovery call to find out exactly what you may be entitled to and how we can help you capture every dollar you’re owed.

You’ve already done the hard part — living with the diagnosis. The free money is supposed to be the easy part. Let’s make sure it is.

This article is for general information only and does not replace personalized financial, tax, or legal advice. RDSP rules, contribution limits, and benefit thresholds are reviewed and indexed annually by the Government of Canada. For current figures, always confirm with the Canada Revenue Agency or a qualified professional.

Related resources for Albertans

Advance Care Planning in Alberta: How a Personal Directive Protects Your Wishes — Once you've secured your financial protections through the DTC and RDSP, the next step is making sure your healthcare wishes are documented and legally protected.

How to Beat Diagnostic Imaging Wait Times in Alberta — For many of my clients, getting the DTC approved starts with getting the diagnostic imaging that confirms their condition. Here's how to skip the line.

What Is a Patient Advocate, Actually? (And What Do They Do?) — A plain-language overview of what we do — and how we help families navigate exactly the kind of bureaucratic puzzle the RDSP represents.

Comprehensive Guide to Patient Advocacy in Canada — A deeper look at how patient advocacy works in Alberta and across Canada, and how to choose the right advocate for your situation.

Empowering Independence Through Home Organization — RDSP paperwork is one piece of a larger puzzle. This guide covers organizing the financial, legal, and medical documents that protect your independence long-term.